- InvestiBrew

- Posts

- 🗞 How I'm Shifting My Portfolio in 2026

🗞 How I'm Shifting My Portfolio in 2026

This is the year of the "value" investor, but don't assume value still means what it once did, because it has changed entirely.

InvestiBrew

January 23, 2026

In partnership with

WHILE YOU POUR THE JOE… ☕️

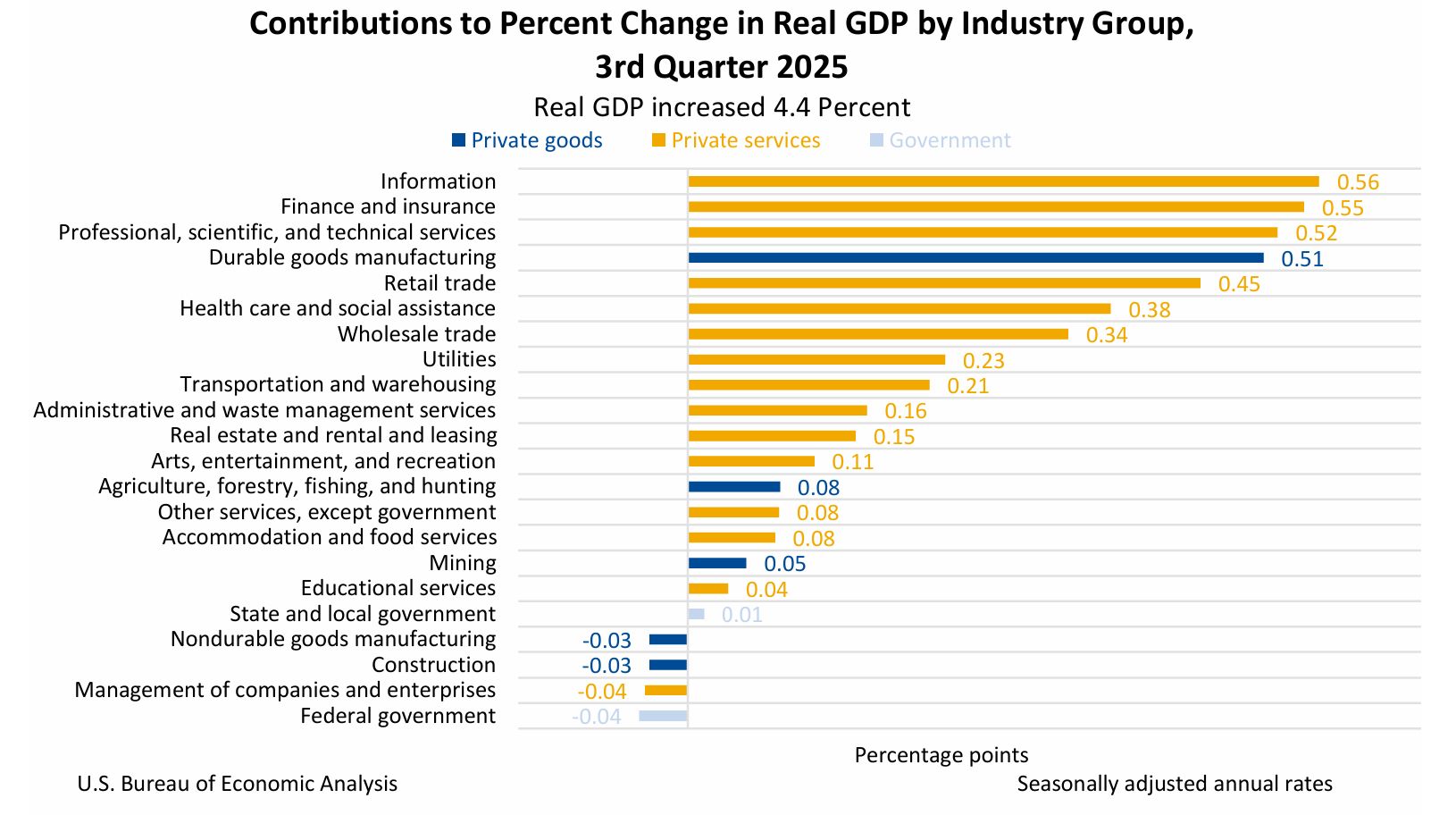

U.S. 3Q’25 GDP Components, Bureau of Economic Analysis

United States GDP is now revised higher to 4.4%, above the previous 4.3% consensus.

Yet the S&P 500 seems to have ignored this new data point, especially as it failed to regain its previous highs.

In my last newsletter, I walked you through how most of the mega-cap names in the market are now trading down to correction/bear market territory.

I also showed you how this is closely tied to where the global liquidity cycle is headed, which matters more than you think.

Today, you’ll be exposed to other important indicators and what they mean for asset allocation and portfolio strategy for this year.

I hope it helps you navigate a potentially volatile market coming up.

Speaking of Strategy for 2026, let’s get on with today’s email 📧…

AI in HR? It’s happening now.

Deel's free 2026 trends report cuts through all the hype and lays out what HR teams can really expect in 2026. You’ll learn about the shifts happening now, the skill gaps you can't ignore, and resilience strategies that aren't just buzzwords. Plus you’ll get a practical toolkit that helps you implement it all without another costly and time-consuming transformation project.

SHIFTING TO DEFENSE

Value is The New Growth

Global Liquidity Cycle, CrossBorder Capital

We already went over how liquidity is starting to top and turn, especially in the United States, as seen in the M2 Money Supply rate of change data. 📉

As noted by CrossBorder Capital, the global liquidity cycle should follow a similar pattern in the first half of 2026.

This is bad for risk assets like Bitcoin and most stocks, especially those with the sort of excess we’ve seen in the AI and Mag 7 space.

Which is leading me to rethink the way I have structured my portfolio up until now, which looks a bit like:

Screen for the Forward P/E premium names

Justify these premiums through above-average EPS growth rates

Overlay with reasonable PEG ratios

Now that liquidity regimes are shifting, taking us back to the 2022 cycle trough, my flagship strategy could underperform.

Let me illustrate what I mean with a lookback to that period:

US M2 Money Supply Rate of Change, InvestiBrew

The Fed was taking money out of the system during 2022; at the same time, the global liquidity index reached its bottom according to the 65-month cycle shown above.

During that time, my “premium” strategy was underperforming even the rookie value investors, which is why I was more heavily focused on buying discounted names like:

PHM

ULTA

SPG

TGT

WSM

Of course, these tallied to double and triple my entries.

Then they suddenly underperformed in late 2024 against some of the market's craziest growth stories in the market.

Here’s exactly why:

IVE/IVW Z-score spread, InvestiBrew

For all of 2022, value outperformed growth, a theme that reversed in 2024 and up to today.

This is why my long/short equity portfolio has run laps around the S&P 500 since then, but it’s now beginning to slow down.

That got me thinking about where I should start focusing next.

Note that, since December, it is a value that has begun to outperform growth almost to the point of parity on the spread.

I can see it live in my portfolio makeup:

Chipotle (CMG)

Dutch Bros (BROS)

Target (TGT)

Just to name a few, these have all outperformed the growth names in the economy like:

Hims & Hers (HIMS)

Coupang (CPNG)

Chewy (CHWY)

Again, just to name a few.

The writing is now very clearly on the wall, and it’s calling for me to shift my thinking and logic around portfolio construction and strategy.

Which, if I can boil it down to a single sentence, would be:

Find high-growth names at a Forward P/E discount to the industry, as long as they also carry a Forward PEG ratio <1.0, ideally.

That’s it in a nutshell. I can go deeper into these themes as we see the cycle accelerate along, but for now, let this show you a better stock picking process, and hopefully, it helps you ignore some of the excess narrative that’s going on right now.

PCE Inflation, InvestiBrew

In other news, we also got PCE inflation numbers yesterday.

The headline number was 2.8% YoY, matching last month's. The problem, though, is that this has now brought up the six-month trend higher into 2.6%.

Remember, the Fed’s preferred inflation measure is 2.0%.

So that’s another way for you to make sense of why liquidity is tightening, and why I am placing more importance on rearranging my strategy and screening process.

Nonetheless:

Client Managed Account, InvestiBrew

One of my most recent clients, for whom I run a managed brokerage account, is still up 11.6% since joining in October 2025.

So, even though this strategy has started to slow down, I can still say there are a few drops of juice left in it.

How and where I will be investing is for another newsletter.

Specifically, my Deal Room members will access all of it first.

To your success,

G 🫰